Dear Readers,

Amine & Plasticisers was recommended @ 49 Rs on 30/07/2017 and today 09/01/2018 touched 109 Rs.......Giving 121% return within 5 months........

Book the profit as my given target achieved today.

Happy Investing!!

Regards,

Kamlesh

===================================

Dear Readers,

Amine & Plasticisers was recommended @ 49 Rs on 30/07/2017 and today 05/01/2018 touched 88 Rs.......Giving 79% return within 5 months........

Regards,

Kamlesh

==========================================

Recommendation: Buy

Hold

for 3 years

Target:

100 Rs.

Date: 30/07/2017

Amines & plasticisers ltd (APL)

By

Kamlesh Bavrva

Company Name: Amines and Plasticizers Limited

CMP: 49

Rs.

BSE

Code: 506248

Market

Capital: 271 Cr.

Face

Value: 2

52 Week

Low / High: 20.8/52.8

Book

Value: 9.8

Dividend (%): 10%

Share Pledge: Nil.

v Amines and

Plasticizers (APL) was incorporated in 1973.

v It

is a small cap company operating in chemical sector and having two

manufacturing plants at Navi Mumbai & Khopoli in India.

v APL

is the pioneer and largest producer of Ethanolamines, Alkyl Alkanolamines,

Plasticizers, Morpholine, Alkyl Morpholines and Gas Treating Solvents in India.

v The Ethanolamines Plant

was set up in the year 1973 under Technical Collaboration with

the erstwhile Napthachemie, France (now a part of British Petroleum) and Plant

Engineering was done by Ralph M. Parsons, USA. For all other products, the

Company has developed the technologies based on its own in house R & D.

v APL

is an ISO-9001:2008, ISO-14001-2004 & OHSAS-18001-2007 Certified

Company.

v APL is a global supplier of organic chemicals

used in Oil Refineries, Natural Gas Plants, Ammonia Plants, Petrochemical

Plants, Pharmaceuticals, Agrochemicals, Textiles, Oil Field Chemicals &

Cosmetics etc.

v In

the field of Ethanolamines and Alkyl Alkanolamines, APL is serving

approximately 75-80% of the total demand of the Indian Market and is regularly

exporting its products to over 50 countries globally including USA, Canada,

Germany, New Zealand, South Korea, South East Asia, Japan, Australia and the

Middle East countries etc.

v In

the field of Plasticizers, APL manufactures a wide range of products which

include Phthalates, Sebacates, Trimellitates, Acetates, Maleates, etc.

v It

is the world third largest producer of N–Methyl Morpholine Oxide, which is the

preferred solvent used for the manufacture of Viscose Staple Fibre by the

Solvent Spun Process. APL's range of Alkyl Morpholines includes Lauryl, Methyl,

Ethyl, Hydroxy Ethyl Morpholines etc.

v APL

has also set–up Plasticizer plants in India and in Pakistan and is currently

executing a turnkey project for a Viscose Rayon manufacturer for the recovery,

regeneration and purification of solvent in the new 'Solvent Spun Process'.

v APL pioneered

the manufacturing of Methyl Diethanolamine (MDEA) in India, an Ethylene Oxide

derivative for which APL was rewarded the highest Award by the Government of

India.

APL

subsidiaries:

v The

amalgamation of APL Engineering Services Private Limited, wholly owned

subsidiary of APL is in its final stages.

v The

fabrication unit of APL Engineering Services Private Ltd. is fully operational

and has been executing various orders for its clients. Also, the Order Book

position of the Company is comfortable for the year.

APL InfoTech Ltd.

v APL

Infotech Ltd’s Pipe leak detection software has been customized and is in the

process of being made operational.

v The

Company is in talks with Gas Transportation Companies in India for installation

of its software on their cross country gas transportation.

Amines and Plasticizers

FZE, UAE:

v APL

Wholly owned Subsidiary:

v The

Company is contemplating expansion of its business operations in the Middle

East and Europe.

v Keeping

in view the said expansion, Amines and Plasticizers FZE in Ras Al Khamaih,

United Arab Emirates for dealing in Specialty Chemicals and other Alkanolamines

products and may opt for manufacturing at an appropriate time.

Export:

v During

the year ended 31st March, 2016, Company’s export earning was ` 9313.40 Lakhs as

compared to `12798.03 Lakhs.

v Exporting

products in near 30 country.

APL Products by Type:

1.Alkyl Alkanol Amines

v

•

2. Alkanolamines

•

3.

Morpholine & Substituted Morpholines

•

4. Specialty

E.O./P.O. Products

•

5.E.O./P.O.

Derivatives

APL Products by Industry:

•

1. Pharmaceutical Industry

•

2. Textile Industry

3. Paints, Coatings, Printing Inks, Polyurethanes, Metal Working Fluids, Corrosion Inhibitors

•

4. Agro Chemicals

•

5. Rubber Industries, Mold Releasing Agents

•

6. Photographic Chemicals

7. Cement Industries

8. Cosmetic Industries

v H2S

Scavenger

v Demulsifier

v Acid

Corrosion Inhibitor

•

10.Acid Gas Treating Solvents

11. Molecular Sieves

•

v APL

is associated with Zeochem for marketing and distribution of their important

products in India on indent basis as well as stock and sale basis

Applications

v Process Industry Applications

1.

Natural Gas Processing

2.

Hydrogen Production or Recovery

3.

Basic Petrochemical and Synthesis Gas

Processes

4.

Petroleum Refining

5.

Industrial Gases

6.

Chemical Storage

7.

Fuel Ethanol Production

8.

Miscellaneous Petrochemicals

v

Industrial Applications

1.

Insulating Glass

2.

Package Protection

3.

Pollution and VOC Control

4.

Polymer Processing

5.

Systems Protection Devices

6.

Medical Oxygen Generation

•

APL Customers:

APL Shareholding Pattern:

APL Share holding Pattern

|

||

% Share holding

|

% Share pledged

|

|

Shareholding

of Promoters & Promoters Group

|

73.16

|

Nil

|

Public

holding

|

26.84

|

|

Total

|

100

|

|

| Financial: |

v Net profit of Amines & Plasticizers rose 106.38% to Rs 4.85 crore in the quarter ended March 2017 as against Rs 2.35 crore during the previous quarter ended March 2016.

v Sales

rose 6 % to Rs 79.47 crore in the quarter ended March 2017 as against Rs 74.07

crore during the previous quarter ended March 2016.

v For

the full year,net profit rose 58.12% to Rs 15.48 crore in the year ended March

2017 as against Rs 9.79 crore during the previous year ended March 2016.

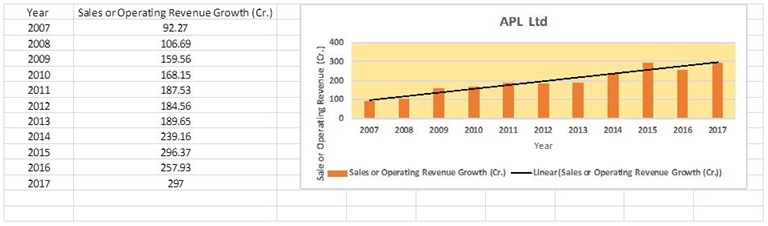

v Sales

rose 13.7% to Rs 297.95 crore in the year ended March 2017 as against Rs 261 crore

during the previous year ended March 2016.

Financial Chart:

Risk Management:

1. Financial Risk.

v The two

major risks in the financial sector affecting the Company are the foreign

exchange fluctuations and higher interest rates on borrowings.

v The

Company is into manufacturing, trading and dealing of various chemicals which

are sensitive in nature. The risks in such product begins from the time of

procuring the raw materials till the delivery of the finished goods because of

the volatility and nature of the chemicals which always needs special care and

attention. The business of the Company is mainly through various tenders opened

by the Government and its companies.

1.

Robust

106% jump in Net Profit

2.

Robust 49% CAGR growth for the 5 years.

3.

13% CAGR Net sale growth for the 5 years.

4.

7% Net sale jumped in 2017 year.

5.

Amines Market worth 19.90 Billion USD by 2020

v Growth in

end-use industries such as personal care, agriculture, water treatment, and

petroleum is the driving the demand for amines.

v Among all regions

included in the report, Asia-Pacific and RoW are estimated to witness a high

growth in the next five years.

v Also, the

demand across these regions is reinforced by the emerging markets, namely,

China, Brazil, and India.

6.

Personal care to be the largest application of amines by 2020

Hence, the rising personal care industry is

indirectly aiding the amines demand.

7. Asia-Pacific is the

major driver of amines market

v In 2015,

Asia-Pacific accounted for the largest market share and is expected to to register

the highest CAGR between 2015 and 2020

v The robust

demand in Asia-Pacific is the major driving factor for the amines market.

v China

registered the highest demand for amines due to increased consumption of across

end-user industries in the last 2-3 years.

v It is also

the largest market for amines at a global level.

v Emerging

economies such as Brazil, India, Mexico, and others are projected to have a

bright future in this market.

8.

Ethylene amines Market worth

$2,138.28 Million by 2019

v The

Asia-Pacific remain the dominating region in the global market with its growing

demand for ethyleneamines in different application segments, especially the

resin, paper, automotive, and adhesive.

v The

Asia-Pacific market is estimated to grow at the highest CAGR in the next five

years, with the allied industries expected to boost the overall business need

in the respective regions.

v Asia-Pacific

is the largest region, both in terms of volume and value, followed by Europe

and North America. India, Russia, Brazil, and South East Asian countries are

expected to continue as successful markets

9.

The global ethyleneamines market was

estimated to be is $1,364.90 million in 2013, and is projected to reach

$2,138.28 million by 2019 expected to grow at a CAGR of 7.81% between 2014 and

2019.

10. The global amines market (2015-2020) is

estimated to reach USD 19.90 Billion by 2020 growing at a CAGR of 8.3% between

2015 and 2020.

11. Growing middle class population in the

developing countries resulting in an increase the demand for the cosmetics,

toiletries and pharmaceutics

12. Growth of the construction industry and

chemical-manufacturing industry as amines are used in masking paints and

corrosion resistant paints

13. Growth of agriculture industry resulting in

increase in the demand for agrochemicals

v Stock is

trading below industry P/E and available

at fair value.

v Stock CMP

is 49 Rs. and stock is trading at P/E 18

& EPS 2.81, Based on above all points stock may touch 100 Rs. within a 3

years’ time horizon.

Please note:

v Note: The

articles are not research reports but assimilation of information available on

public domain and it should not be treated as a research report.

Registration status with SEBI: I am not registered with SEBI under the (Research Analyst) regulations 2014 and as per clarifications provided by SEBI: “Any person who makes recommendation or offers an opinion concerning securities or public offers only through public media is not required to obtain registration as research analyst under RA Regulations”

Disclosure: It is safe to assume that I might have the discussed companies in my portfolio and hence my point of view can be biased. Readers should consult registered consultants before making any investments.

Registration status with SEBI: I am not registered with SEBI under the (Research Analyst) regulations 2014 and as per clarifications provided by SEBI: “Any person who makes recommendation or offers an opinion concerning securities or public offers only through public media is not required to obtain registration as research analyst under RA Regulations”

Disclosure: It is safe to assume that I might have the discussed companies in my portfolio and hence my point of view can be biased. Readers should consult registered consultants before making any investments.

The first phase the preparation should, theoretically, be uninfluenced by the intended intensity and duration of the sound which is subsequently produced. In fact, however, so quickly are the three phases accomplished that the pianist rarely has capacity to think, in performance, of each phase separately. Buy 5fadb powder

ReplyDelete